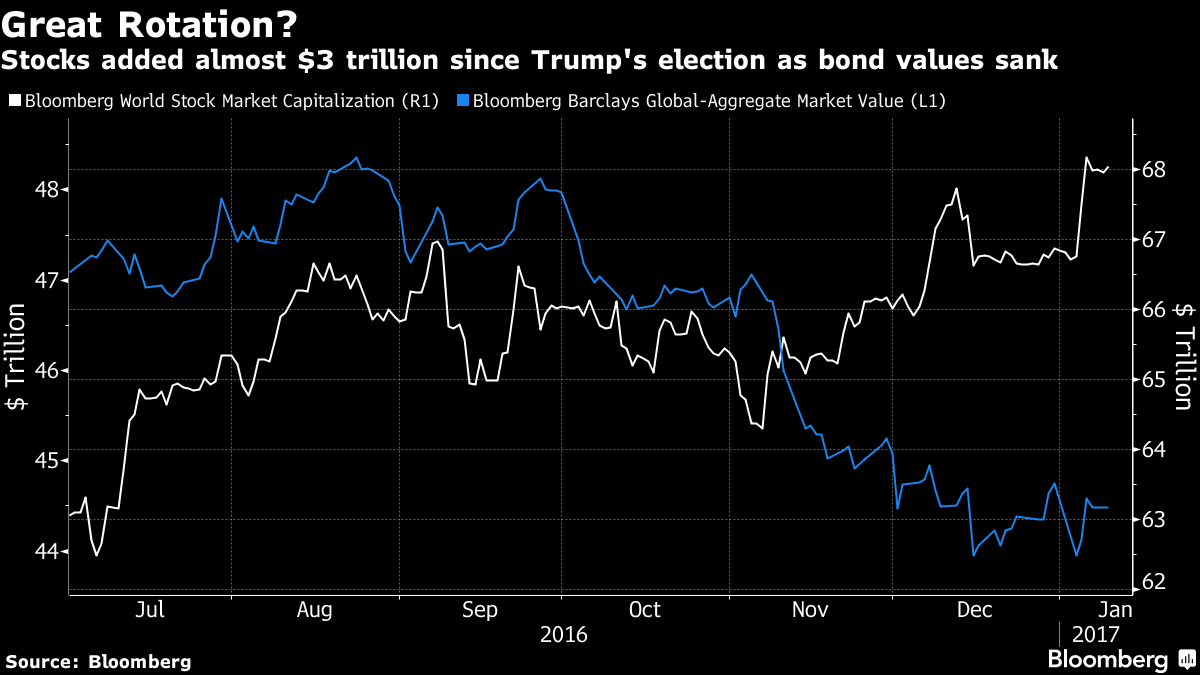

Equity markets around the world roared to a strong year-end finish by posting healthy gains in December as the after-glow of the US Presidential victory by Donald Trump continued. The Australian share market improved an impressive 4.4% with gains spread fairly evenly across both the industrials and resource sectors. For the calendar 2016 year, Australian shares returned a healthy 11.6% including dividends. The beleaguered A-REIT sector, which had been hit by the recent rise in bond yields, staged a sharp recovery posting an impressive gain of 6.8% for the month. In overseas markets, European shares were particularly strong led by Germany up 9.5% while the UK shrugged off Brexit uncertainties to be up 5.4%. The US market advanced 2% building on the solid gains recorded in November, posting a healthy gain of 9.5% for the year.

Emerging markets faired worst due the impact of the strong USD and the fears of the possibility of trade restrictions with the US. The Chinese market was down 5.9% as most of the trade rhetoric from the President-elect has been directed towards them given the large trade deficit between the US and China. Following the sharp sell off last month, bonds were more or less flat in December despite the US Fed raising cash rates by 0.25% as expected. The Australian 10 year bond yield closed at 2.77% with its US counterpart finishing the year at 2.45%. The oil price strengthened on the back of OPEC’s plans to cut production by 1.2 million barrels a day over the first half of 2017 and finished the year 45% stronger. Bulk commodities also posted strong annual gains with iron ore up 85% and thermal coal up 87% coming off very low bases at the close of 2015. The surge in the USD continued as it rose against the major crosses and advanced 2% against the AUD on expectations of a narrowing interest rate differential based on divergent monetary policy directions between the two countries.