Share markets around the world put in a solid performance in February building further on gains in recent months. The “Trump Reflation” effect has ignited the animal spirits of the US market, which advanced 4% following 12 straight days of new highs towards the end of the month. European markets were also strong led by the UK up 3.1% and Germany up 2.5% however France was flat as the market was gripped by the uncertainty surrounding the first round of the Presidential election to be held on April 23rd. Across Asia, China and Hong Kong were up just over 2% on positive Chinese data however Japan was flat driven by a weaker Yen.

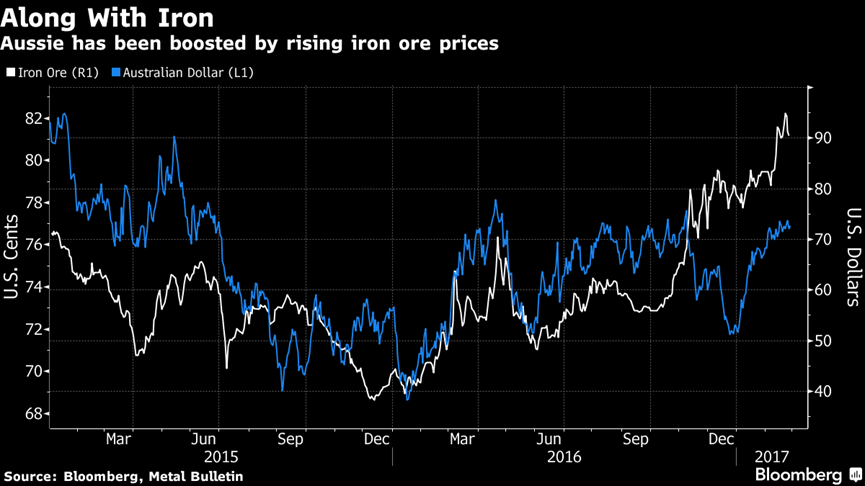

The Australian market was up 2.2% buoyed by a stronger industrials sector as investors digested first half FY17 earnings results. REIT’s had a strong month up 4.3% as positive asset valuations over the half saw NTA’s rise by 5%. The AUD was 1 cent stronger against the USD as rampant iron ore prices (up 12%) drove the local unit higher. Bond markets were a little firmer with the Australian 10 year bond yield falling 7bp with the US equivalent falling 12bp despite the prospect of tighter monetary policy ahead.