Markets not out of the woods yet

Despite the positive tone so far in 2019, there are still risks that we need to be cognisant of. While there have been positive announcements about the progress of trade talks between the US and China ahead of the 1 March deadline for further tariff increases, the devil may well lie in the detail of any deal. We expect that China will commit to buying more US agricultural exports as a means of reducing the trade deficit, however, a resolution on the more structural issues such as forced technology transfer, theft of intellectual property and cyber espionage may well prove more problematic. It remains to be seen what kind of trade deal will appease the market, however, a “no deal” and further increases in US tariffs on Chinese imports will be unequivocally negative.

Outside of the US, economic conditions are not as rosy, especially in China where the government has introduced a number of stimulatory measures to bolster growth. The problem is that these measures are adding to the debt burden already plaguing the economy. The challenge for the Chinese authorities is to manage the deleveraging of the economy while still maintaining their targeted level of growth. The European economy has been slowing for some time, especially in the manufacturing hub of Germany. The conundrum for the ECB is how to normalise liquidity conditions against the backdrop of a weakening economy. Adding to the uncertainty on the continent is the messy situation regarding the UK’s “Brexit” from the European Union. British Prime Minister Theresa May is finding it difficult to strike a deal that is acceptable to both the European Commission and the British Parliament while consistent with the 2016 UK referendum. With the March 29 deadline to exit the EU looming, it is hard to fathom what the ultimate outcome will be which is casting a pall of uncertainty over financial markets in the region.

Investment Outlook

As we often emphasise in these reports, we take a strategic approach to setting the appropriate asset allocation strategy for our clients. We look though sentiment driven market noise, preferring to focus on the fundamentals that ultimately drive markets over longer term periods. Our objective is to always strike the appropriate balance between risks and opportunities. In response to elevating risks over the course of 2018, we took steps to de-risk diversified portfolios by reducing exposure to equities in favour of more secure assets such as government and corporate bonds. The change in the monetary policy stance in the US and Australia is a good example of a change to medium term fundamentals which will provide good support for risk assets such as shares. Prior to this development, our bias was to further de-risk portfolios, however, as a consequence of this development we are much more comfortable with the equity positions we currently hold.

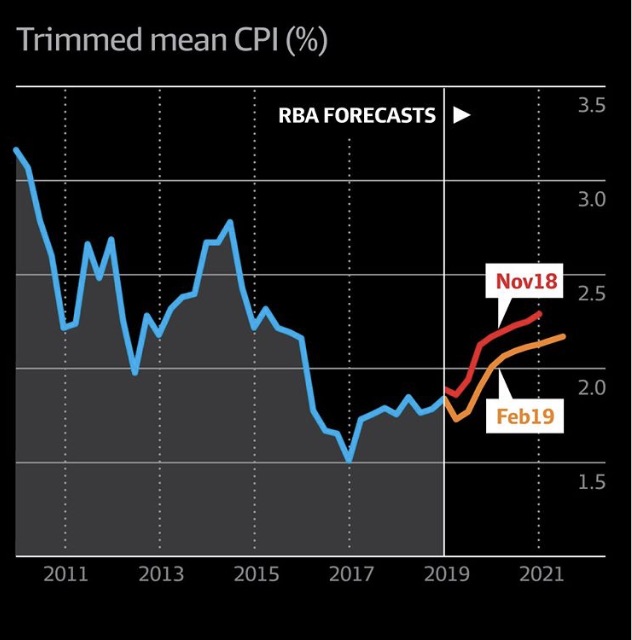

While government bonds are often viewed as a staid and boring asset, they provide a high degree of security and excellent mitigation against the higher risks of holding equities. With the RBA unlikely to raise rates this cycle, the outlook for bonds has improved, further enhancing their appeal in a diversified multi-asset portfolio. With the AUD often considered a risk proxy currency, a healthy exposure to foreign currency, especially the USD, also provides excellent risk mitigation.