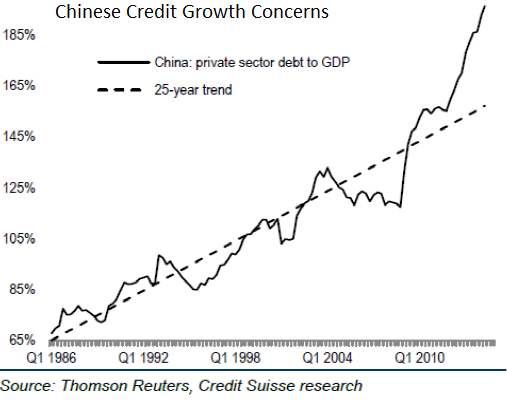

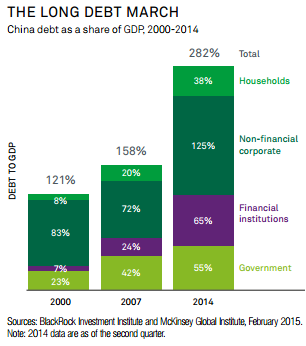

In summary – China does look concerning on many metrics, however we believe the government has the fiscal capacity and control of enough levers to smooth passage of necessary economic reform, at least for the short to medium term. Having said that it seems likely that volatility in China’s economic data and markets will continue as it attempts to manage this process, and as it deals with its growing debt pile. This will likely continue to feed in to global asset markets. And if the situation changes to one of sudden deterioration the impact is likely to be far-reaching given the scale of credit growth. We remain vigilant to this risk, and are closely watching the current equity market volatility in China.

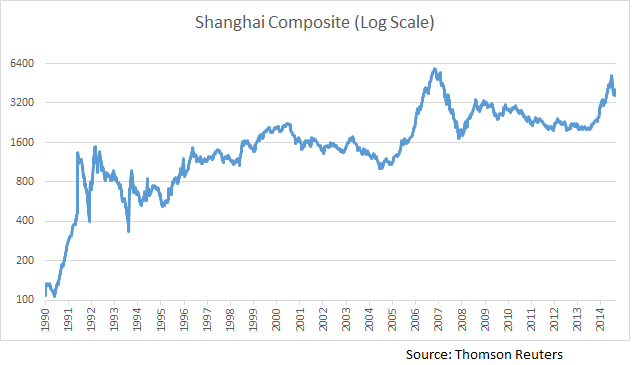

At the end of July Chinese stocks were down 28% from their peak in June, though are still up 66% over the twelve months since July 2014. The market had largely traded flat since the financial crisis. To put this pullback in perspective the current bear market is only one of 27 seen over the last 25 years, and is only the 20th worst. In the two years after China opened its stock markets, shares soared 1,200% and twice fell by half. Investors seeking IPO shares rioted, overturning cars and smashing windows, leading police to use tear gas and fire their guns in the air to quell the disturbance.

In an attempt to arrest the current equity sell-off China put a curb on new share issues, orchestrated brokerages and fund managers to purchase stocks, banned major shareholders from selling for six months, and at one point put over half the stocks in to a trading halt. However whilst these measures may have eventually succeeded in stabilising the market, though even this assertion is up for debate, the whole episode has highlighted the limits to state power as markets kept dropping despite the government drawing various lines in the sand. This is, in part, due to the structure of the Chinese market which is 85% retail. This compares to most other markets which are dominated by institutional investors.

There has been some concern in the media that the stock market rout could spill over in to the real economy. Margin debt reach a record 8% of the market’s free float according to Macquarie research, and brokers opened four million new accounts in a single week in April. However given the speed of the boom and bust, the fact that many shareholders are still sitting on profits, and the relatively small percentage of GDP that the stock market represents, we don’t believe the immediate impact will be large. Perhaps the bigger concern is that this represents a stalling of China’s reform agenda, which we believe is essential to ensure stability of growth going forward.

Greece – Rabbit out of the Hat

In the Greek referendum 61% voted to back Tsipras’s rejection of further austerity. Only 38.7% voted for “yes”, despite polls showing an even race (the rest were invalid). It didn’t take long for the festivities held on the night of the vote to give way to the reality that the referendum didn’t change anything. Whilst Tsipras may have had a democratic mandate to end austerity, the other countries in the Eurozone certainly did not. Subsequent to the vote the outspoken and hectoring finance minister, Varoufakis, quit. He was replaced with a more conciliatory minister, though equally of a Marxist persuasion, who at the first restart of negotiations read out a list of suggestions scrawled on a bit of paper from the hotel he was staying in. At this point it seemed extremely unlikely that the Europeans would come to an agreement, and indeed the creditor countries more or less told Greece to prepare for exit. We had always been of the opinion that an eleventh hour agreement would be reached, but in that final week this looked unlikely.

However in true European style a rabbit was pulled out of the hat at the final stretch. After 17 hours of negotiations over the weekend before Greece was to be ejected Tsipras conceded to a deal that was for worse for Greece than anything put on the table previously. In exchange for a new bailout package worth up to EUR 86bn, as well as around EUR12bn of short-term bridge financing, Tsipras agreed to the following, basically a wish-list of creditor country demands:

- EUR 50bn of state assets to be transferred to a holding company that will seek to either sell them or generate income. This will be based in Greece, but under “EU supervision”.

- Proceeds will be used to recapitalise the banks, pay off the debt, and invest in Greek infrastructure

- A debt haircut was declined but longer maturities and interest free periods will be discussed.

- Pension reform, including deep cuts

- Improved VAT collection and broaden the tax base

- New retail laws, free up Sunday trading rules

- Create a system of “quasi-automatic” budget cuts in case the Greek economy underperforms

- Privatisation of the electricity grid

- Weakening of trade unions

- Reform of the Greek judicial system

- The European Commission will try to mobilise €35bn – outside the ESM loan – to help Greece with growth and job creation

Greek legislators had to enact various measures in the week following the agreement. These passed with support from the opposition and major dissent within Tsipras’ own Syriza party. It seems likely that new elections will need to be held soon, though not until the details of the agreement are agreed and put in place, which will likely take a couple of months. The great mystery is that Tsipras has brought the Greeks a terrible deal and maintains an approval rating over 60%. Apparently voters blame his negotiating partners, and feel he stood up for them. If snap elections were to happen now, 42.5% of Greeks would vote for the Syriza party, nearly double the level of support for the main Centre-Right opposition party, New Democracy, at 21.5%, according to a survey published by polling company Palmos Analysis. Amazing.

The Other Big Deal – Nuclear Agreement

The other major geopolitical event last month was the conclusion of a nuclear deal between Iran and the U.S., Britain, China, France, Germany and Russia. Iran will reduce the number of centrifuges by two thirds, and IAEA inspectors will be allowed access in perpetuity with heightened inspections for 20 years. It is estimated the actions will take Iran from being able to assemble its first bomb within 2-3 months, to at least one year. Talks have spanned 20 months, and may lead to the restoration of diplomatic relations which have been severed since 1979. The deal was subsequently approved by Iran’s parliament, and perhaps more importantly by the Supreme Leader Khamenei. This was despite various red lines he laid down being crossed, perhaps he was simply hedging his bets. The U.S. congress has 60 days to approve the deal, a Democratic rebellion seems unlikely so we think the deal will get across the line. This may have an impact on the oil market as Iran could in theory pump up to an extra 1m barrels of oil a day, though this will take time and investment to bring on line. It is also likely to reshape politics in the Middle East for years to come.

Australia – Waiting for Investment

A rate cut in May did little to lift lending in Australia, with finance down a seasonally adjusted 1.3%. On the other hand the NAB monthly survey showed business confidence rose to its highest level since September 2013. Presumably this is due to the impact of lower rates, a lower dollar, and a better budget than expected. However it is still hard to reconcile with Australia’s business investment plans, which look terrible. We would want to see investment spending rise before turning more confident on Australia.

Despite low rates and the dollar’s drop there are structural impediments to boosting investment. Labour costs that doubled in the decade to 2001 have left Australia with the smallest manufacturing sector as a proportion of GDP among countries in the OECD. Australian businesses currently expect to dedicate just 6% of their long-term capital spending to manufacturing, or $6.27bn, down from a peak of 28% in 1992, according to government data. That’s less than BHP has budgeted to upgrade just one of its pits, the Escondida copper mine in Chile.

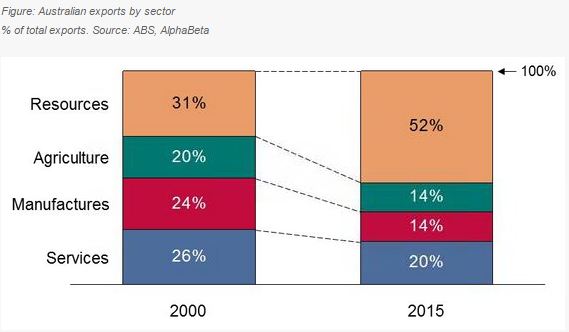

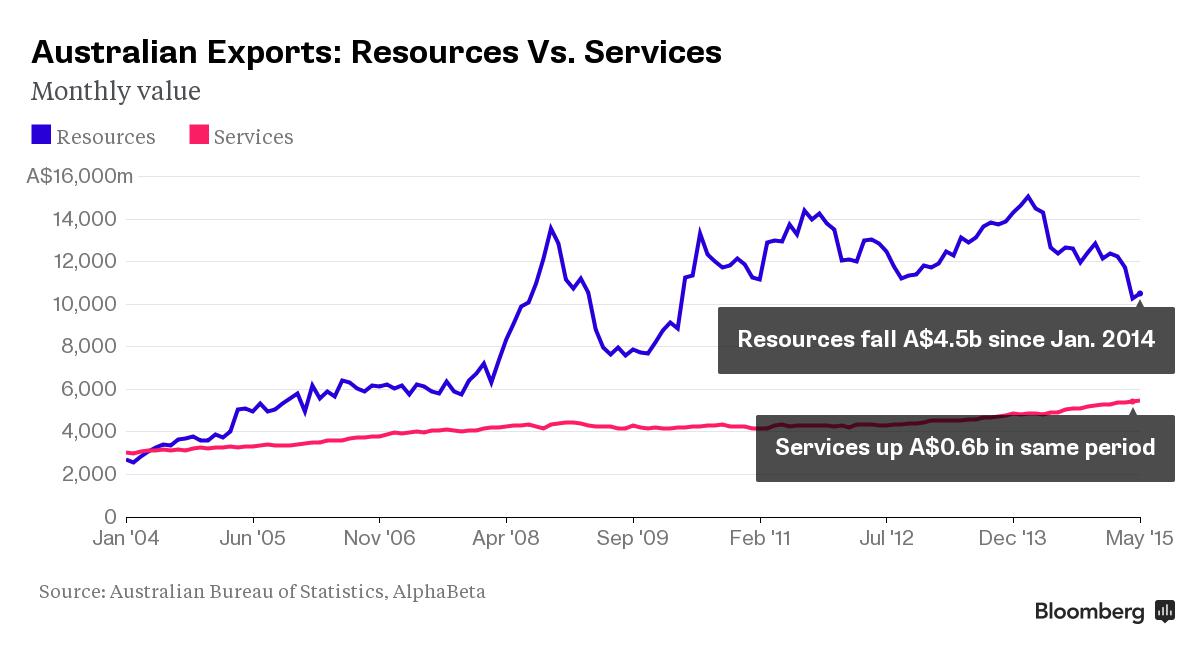

The concentration of shipments abroad is at the highest level in more than 50 years, according to Andrew Charlton, who counselled former Prime Minister Kevin Rudd on economic policy. Even some low-income countries like Nepal, Kenya, and Tanzania have greater export diversity than Australia. The nation’s budget is “hostage” to global iron ore prices, with a $10 drop taking up to A$10 billion from forecast revenue, he said. Resources account for more than half of Australia’s exports, the country’s shipments picture is more like that of a low-income country than it has been in decades.

Commodities – Still Falling

Iron ore prices have rebounded from the lows of the month, though the commodity complex still looks to be under pressure. Many base metals are at three to six year lows. Essentially we are in a period of oversupply following massive investment during the boom of the Supercycle. As we have discussed China is now slowing down, and global demand remains week. This, coupled with a market that is re-focusing on Fed rate rises, has led to soft commodity prices and a soft AUD.

Meanwhile the International Energy Agency (IEA) found that the world remains “massively oversupplied” with oil. The IEA doesn’t expect the market to tighten until next year when output growth in the U.S. begins to stagnate in mid-2016, meaning prices may have further to fall. Since October the number of rigs actively drilling for new oil globally has declined about 42%. More than 70,000 oil workers have lost their jobs. And in 2015 alone, listed oil companies have cut about $129 billion in capital expenditures. However whilst U.S. production has levelled off since June, OPEC continues to pump more oil, as can be seen in the production figures above.

Discretionary Portfolio Changes

In the Australian portfolio we executed the following trades:

| Date |

Stock |

Trade |

Remarks |

| 31-Jul-15 |

CSL |

-1.3% |

Reducing position to take profits. |

| 31-Jul-15 |

NVT |

1.0% |

Adding to position after results, still like the story. |

| 22-Jul-15 |

ENE |

-1.1% |

Exiting position after takeover bid launched. |

| 22-Jul-15 |

IPL |

1.1% |

Adding to position after recent pullback. |

| 21-Jul-15 |

ENE |

-1.2% |

Exiting position after takeover bid launched. |

| 2-Jul-15 |

AIO |

-1.0% |

Reducing position after takeover bid launched. |

| 2-Jul-15 |

ANZ |

-5.7% |

Exiting position as ANZ has biggest question marks over capital position. |

| 2-Jul-15 |

BSL |

2.4% |

New position – stock is cheap and restructuring could unlock value. |

| 2-Jul-15 |

WBC |

4.3% |

Increasing position with funds from ANZ sale. |

| 1-Jul-15 |

MQA |

1.2% |

Increasing position at attractive entry level. |

| 1-Jul-15 |

TCL |

-3.9% |

Exiting position to take profits. |

| 1-Jul-15 |

TPI |

1.0% |

Increasing position at attractive entry level. |

In the International Value portfolio we executed the following trades:

| Date |

Stock |

Trade |

Remarks |

| 27-Jul-15 |

LeGrand |

-3.8% |

Reducing position to take profits as stock has approached our fair value. |

| 27-Jul-15 |

Bunzl Plc |

3.8% |

New position – see note. |

| 27-Jul-15 |

Praxair |

-1.0% |

Reducing position due to current headwinds for business. |

| 27-Jul-15 |

Fiserv |

-0.5% |

Reducing position to take profits as stock has approached our fair value. |

| 27-Jul-15 |

Compass Group |

1.0% |

Increasing position at attractive level. |

| 27-Jul-15 |

3M |

0.5% |

Increasing position at attractive level. |

Bunzl is a multinational distribution and outsourcing company. It supplies to other businesses non-food products that they use in their operations but do not sell. These include food packaging, cleaning and hygiene supplies, personal protective equipment and carrier bags. 80% of the cost to the customer of these items is in the administration, warehouse space, handling cost and special equipment. Bunzl can typically save the customer 10-15% on the purchase cost alone, and provides considerable benefits in these other areas. Bunzl’s customers include contract cleaners, retailers, catering firms and food processors.

Bunzl operates in a fragmented industry with many small competitors but very few national operators in any country. As such, for large customers that have decided to outsource these supplies Bunzl has no effective competition. Bunzl spends essentially all of its free cash each year on bolt-on acquisitions, either to enter a new category or territory, or to add capability to an existing geography. Bunzl is usually the only bidder, and has consistently paid an average of 7.5x trailing EBIT for acquisitions, which we view as highly attractive. Bunzl is currently trading on 20.5x trailing cash earnings and a material discount to our appraisal of intrinsic value.

Please be in contact if you wish to discuss any of these themes further, or wish to make any changes to your portfolios.