Greece – a Progress of Sorts

A broad economic reform plan for Greece won the approval of Eurozone finance ministers and governments. It seems likely, however, that the friction will continue as the details are debated over the course of the year, and as the Syriza leadership butt up against the hard-left of their party. Meanwhile Greece’s finance minister raised the possibility of a referendum or elections to approve the outcome of negotiations. The last time Greece said it would seek a referendum on bailout terms, in 2011, the prime minister was ousted and global markets panicked.

Advance Australia?

Australian Quarterly Wage Growth / Reuters

In Australia the economic data remains unconvincing. GDP data was released for the final quarter of 2014, the 0.5% quarter-on-quarter pace was the slowest since the middle of 2013. Household spending picked up strongly, growing by 0.9%, but non-dwelling construction fell, bringing the total annual decline to 9.1%. The wealth effect apparently continues to support consumer spending, despite constrained wage growth. Wages rose 2.5% last year, which is the lowest growth for 17 years. On the one hand this is a negative, as it constrains consumer spending, on the other hand it is an essential element to Australia’s bid to regain competitiveness. Meanwhile, the terms of trade for the year fell nearly 11%, bringing the total decline since the export price peak in 2011 to more than 25%.

Furthermore an Australian capital investment survey found mining companies will cut investment next financial year by 20%, manufacturers by 20%, and the rest of business by 7%. That would be the worst investment results in 5 years. Capex was also revealed to have fallen 2.2% in the Dec quarter. One thing is clear – if these trends continues there is only more support for the RBA to cut rates further. Though low interest rates have not yet produced any pickup in business confidence, the NAB survey dropped 3 points to zero in February. This is well below the long-run average, and is at its lowest point since the 2013 federal election. We continue to remain cautious on the Australian economy, though believe further rate cuts from the RBA will support the market in the short-term.

China Slows

Chinese Premier Li Keqiang said his government has scaled back the growth target for 2015 to around 7%, which would be the slowest rate of expansion in 24 years. This was in line, or at the top end, of market forecasts. This year China will focus on liberalizing banking and the financial markets, reforming state-owned businesses and fighting corruption, he said. It is always a question of how much of a slowdown in growth the government is willing to stomach in order to enact necessary reform. The slowdown certainly continue apace. Industrial production grew at a 6.8% annual pace over the first two months of the year, well below estimates, and industrial profits were down 4.2%. The value of property sales also fell 15.8% in the first two months from a year earlier. House prices were down 5.7% year-on-year according to Reuters, accelerating from January’s 5.1% decline. In February export orders shrank at their fastest rate in 20 months. The list goes on. All this comes despite figures for lending coming in above expectations. Loan growth actually slowed to $163bn in February, down from $235bn in January, though the $235bn pace set in January was the strongest since mid-2009.

We continue to believe that the slowdown is beyond the government’s comfort zone, and that further stimulus will be carried out. This will buoy markets in the short to medium-term, but in the longer term the combination of exploding debt and slowing growth makes us nervous.

The Curious Case of the United States Consumer

The run of soft data, outside the labour market, continues in the U.S. factory production slipped 0.2% last month after declining 0.3% in January. The market was hit hard off the back of durable goods falling 1.4% in February from a month earlier, versus expectations of a 0.2% rise. January’s orders were also downgraded to a 0.1% contraction, from the previously reported 0.5% rise. The last time durable goods rose was in August, this all points to soft business spending plans. No doubt orders have been impacted by the rising dollar, the West Coast ports strike, and possibly the classic bogeyman of the weather.

U.S. Monthly Home Sales / Reuters

Meanwhile retail sales fell 0.6% in February, marking the third month in a row of declining sales, expectations were for a 0.3% rise. This comes despite a buoyant jobs market, with jobless claims dropping to 282,000 and unemployment at 5.5%. In addition the housing market remains reasonably solid with prices up 4.5% year-on-year, and new-home sales rising to the highest level in seven years in February to an annualised rate of 539,000 homes. However we believe that in a true bull market for construction this number would be closer to 1m houses built a year. In addition lower petrol prices have delivered a substantial effective tax cut. U.S. consumers are saving the windfall, the savings rate has increased to 5.5%, the highest in two years. This presents a bit of a conundrum, though perhaps missing wage growth which is still the key element.

All these data points have prompted economists to drop their estimates of first quarter GDP by as much as 0.6%, to as low as a 1.2% annual rate. And the case is building for the Federal Reserve to delay a planned boost in interest rates. We believe that whilst this is the case that support for the U.S. market will remain.

Europe – Green Shoots Continue

Data out of Europe continues to improve, albeit from a very low base. It appears that unlike the United States, where consumers have been saving more, European consumers remain happy to increase spending in light of declining petrol prices. This, and the fastest real wage growth since data collection started in 2008, has prompted German business confidence to rise to a seven year high of 106.8 in February. The Eurozone’s combined PMI climbed to 53.7 in February for one of the best readings in years. Germany powered much of the growth, but France also registered its best performance since 2011. GDP growth in the Eurozone was also up 0.3% in Q4 versus 0.2% in Q3. We remain encouraged by European data though are watching closely as European valuations continue to close the gap on U.S. shares.

Equities

In Australia the major theme in the market remains the RBA’s easing bias and the hunt for yield. A major beneficiary of this dynamic has been the banking sector. UBS notes that it now makes up 32% of the ASX 300, the largest exposure of any banking sector of any developed market exchange in modern history. UBS also notes that the sector’s forward PE multiple of 15.6X is unprecedented. Though that probably won’t stop bank stocks rising further if the RBA continues cutting, relative to bonds the div yield still looks compelling. This of course means that valuations are likely to correct when rates start rising, though we don’t foresee that in Australia for some time, however a Fed tightening cycle would have some impact also.

Meanwhile dividend growth in Australia was more than double that of earnings in the February reporting season. The payout ratio rose by around 5% to 65%. Dividends grew by 5% for the six months to December, whilst earnings were up only 2%. This may be pleasing for the yield trade in the short-term, but increases the chances of dividend cuts, and a correction, when the cycle turns. The percentage of companies upgrading their profit forecasts was low by historical standards, at 42%. We continue to remain cautious on valuations in Australia, though in the short-term the market is likely to be supported by the RBA.

In the U.S. analysts have been downgrading their estimates for corporate earnings in the quarters ahead, due in large part to the strong dollar. Profits are now expected to grow only 1.9% this year, down from an expected growth rate of 8% in December, and 11.6% in September. First-quarter profits are expected to fall by 4.9% from a year earlier. The last time analysts cut their outlook on annual profit growth by that much was in the six months leading to March 2009, according to FactSet, as stocks were tumbling to their crisis-era lows. And should profit growth come in at the 2.1% rate for all of this year, it would be slowest pace of earnings growth since profits shrank 7.9% in 2009. We believe that with underlying fundamentals for the U.S. economy remaining broadly positive that low expectations represent an opportunity.

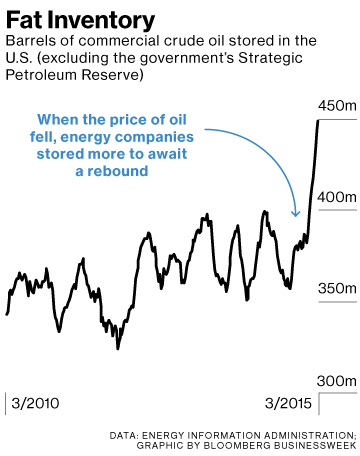

Oil – a Slippery Slope?

Oil prices have continued their slide, with front month WTI futures trading below $44 at one point before rebounding at the end of the month. The market took fright that inventories are still building. The amount of oil stored at Cushing has almost tripled since October, to more than 51 million barrels, that is the fastest increase on record. In mid-March nationwide stocks were at 449 million barrels, by far the most ever. However according to the EIA the U.S. is using a somewhat moderate 63% of its storage capacity, up from 48% a year ago. Though elsewhere I have read that storage facilities in the Midwest are about 70% full, while the East Coast is at 85% capacity. In any case the trend appears alarming for the oil price, but how much inventory build is already priced in?