Following the strong returns delivered in the first 2 months of this year, markets consolidated during March with shares in major regions closing slightly higher. The V shaped recovery so far this year has been impressive and virtually all the losses suffered in the closing months of 2018 have now been recouped. The US improved by just under 2% driven by the rosier interest rate outlook provided by the Fed, Europe advanced by 1.3% mainly due to a stronger French market as the region’s largest economy Germany is teetering on recession pushing shares down 0.7%. The UK rose 2.4% on optimism the Brexit saga would finally be resolved while China rose 3.2% on hopes of a resolution to the trade war with the US together with some encouraging manufacturing data.

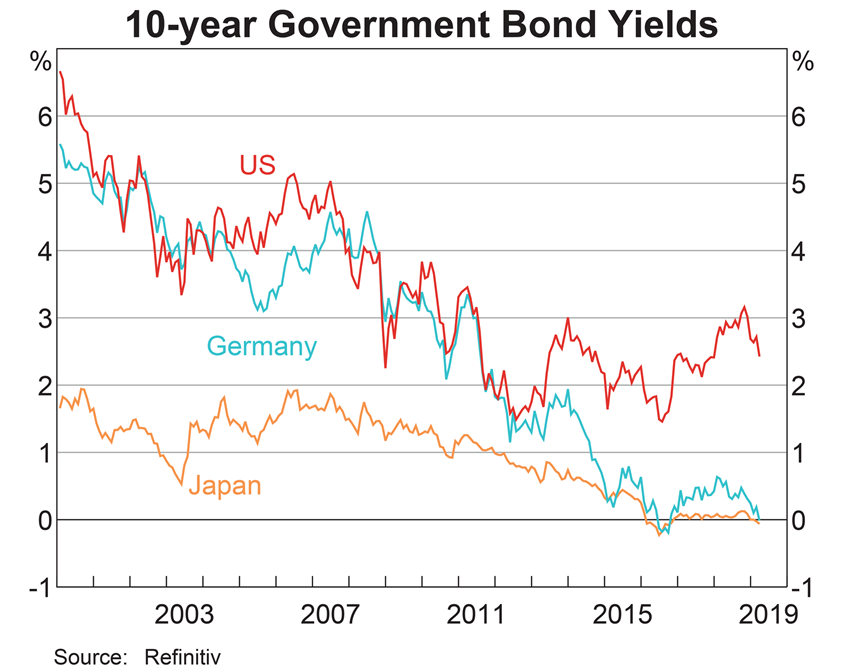

In Australia, our market edged just 0.7% higher propelled by a stronger resource sector fueled by higher commodity prices while the bond rate sensitive Real Estate Investment Trust (REIT) sector was the stand out, posting an impressive 6.2% gain. Bond markets caught fire during the month reflecting the change in the monetary policy outlook for the world’s major central banks. Australian 10 year bond yields fell by 33bp to finish the month at a record low yield of 1.78% while in the US 10 year treasury yields fell 31bp to close at 2.41%. The AUD has proved stubbornly resilient hovering around 71c against the USD with the positive impact of a stronger iron ore price offsetting the negative effect of a forecast widening interest rate differential between Australia and the US.