Returns for the month of September:

Global Growth and Trade Concerns

We have discussed in previous reviews how the slowing of China’s economic growth, and of emerging markets in general, has impacted global growth rates. Aside from the direct impact on global growth the associated decline in commodity prices has also been an important dynamic. According to Credit Suisse, commodity-related capex accounts for around 30% of global capex. They estimate that the 13% decline in oil capex, and 31% decline in mining capex over the last 12 months, has taken around 1% off global GDP. In addition to this there have been large rounds of redundancies in the sector, meaning a subset of employees are spending less.

Of course lower commodity prices, in particular oil, should produce greater consumption and even increased investment over time in projects where commodities are a large input cost. In the longer term lower commodity prices tend to boost growth as commodity-consuming countries spend and invest the savings more readily than commodity-producing countries, which tend to save a higher portion of any windfall. For oil in particular the IMF estimates that the fall in price should eventually boost global growth by around 0.5% to 1.0%, even accounting for lower capex. However in the first instance commodity-producing corporates have acted more rapidly, the boost from consumers may take longer to arrive.

Another key concern for the global economy has been the slowing of global trade. South Korea, a forerunner for the global economy, saw its exports fall 15% year-on-year in August. Chinese exports were down over 5% over the same period. The CPB Netherlands Bureau for Economic Policy Analysis, a group that monitors global import and export volumes, found that world trade had declined over 3% in May from its December peak. This was the sharpest fall since the financial crisis, though trade has rebounded somewhat since then.

Looking over a longer time frame, trade has generally grown faster than global GDP. This was especially true in the 1990s as liberalisation in China and the former Soviet Union, the creation of the WTO, and the expansion of global supply chains, saw a rapid expansion. From the mid-1980s until the middle of last decade annual trade grew at 7% per annum. However since the financial crisis trade has generally been growing at or below GDP growth levels. To be fair part of the recent decline in trade has been due to a rising US dollar reducing the notional value of goods traded in other currencies. If you look at volumes, trade was still growing at 1.7% year-on-year in the first half of 2015. Though this is down from a long-term average of around 5% a year.

What has been driving this recent shift? Partly it has been Europe, which is responsible for 25% of global GDP and one third of global trade, and has been growing only weakly. Clearly China’s demand for raw materials is declining as it transitions away from investment to consumption. And one-off factors such as the recent West Coast ports disruption in the US have played a hand. But structural factors have also played a part as America takes step to energy independence, and China in-houses much of its supply chain. In addition rising incomes in emerging markets, particularly China, has meant that manufacturing some goods in their end markets is once again becoming economic. In 2013 Lenovo, a Chinese PC-maker, opened a factory in North Carolina.

We believe it is still too early to make a call on whether the recent softness in global trade is part of a longer-term trend, or whether it is part of a more typical cycle. We will be watching the space closely, though one event which may be positive for world trade in the future was the recent agreement on the Trans-Pacific Partnership (TPP). A breakthrough compromise on protections for new drugs brought the 12 nations TPP negotiations to a successful conclusion. It represents the biggest trade deal in 20 years and should provide a positive sentiment boost, though we will wait to see the details in a few weeks. Australian farmers should get a major boost with tariffs for beef, dairy, wine, sugar, rice, horticulture and seafood slashed. This includes the export of rice to Japan for the first time in 20 years, and a doubling of the amount of sugar to be exported to the US. In both these cases the amounts were not as high as hoped, but are certainly an improvement on the current situation.

The Fed Holds Fire

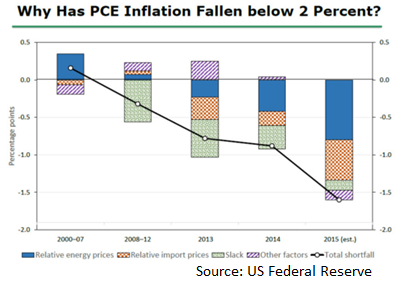

Citing the persistence of downward pressure on inflation, the US Federal Reserve left its policy rate unchanged in September. It seems likely that global economic uncertainties and market turmoil also tipped the scales towards a more dovish stance in what is a finely balanced decision process. On the one hand inflation remains low. Indeed the Fed has downgraded its own inflation forecasts from the June meeting.

However as can be seen in the below graph, much of the recent decline in inflation is estimated to have come from reduced energy prices and the rising US dollar, both of which are likely to be transient factors.