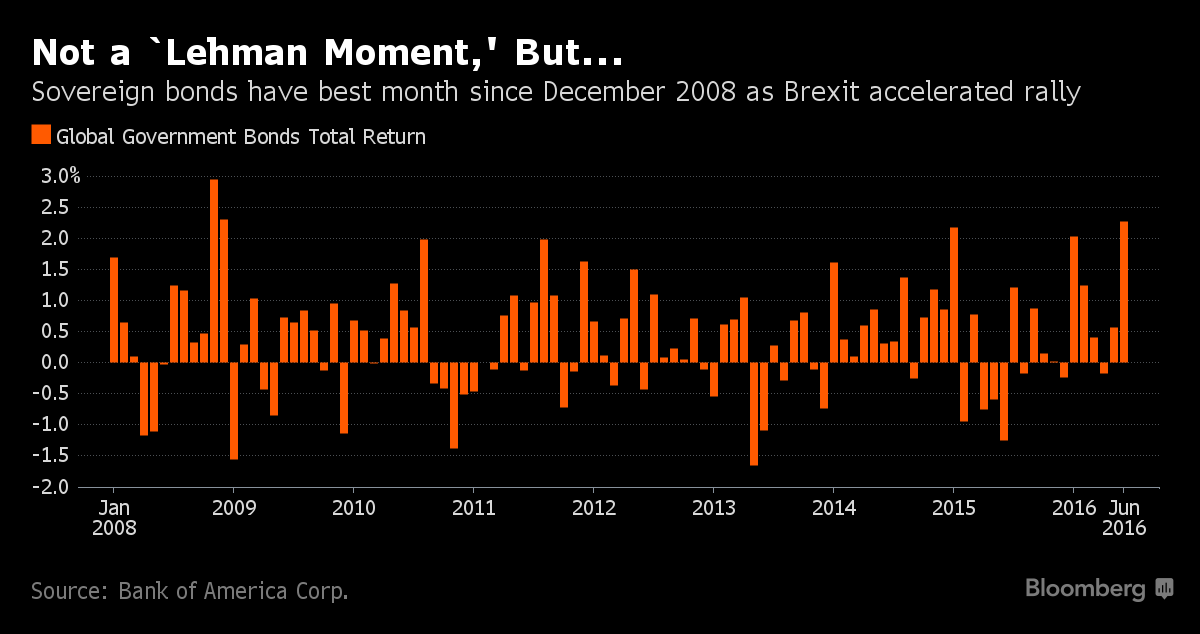

The final month of the Australian financial year proved to be a tumultuous one for financial markets culminating in the UK referendum, which surprisingly resulted in Britain deciding to leave the European Union. Market reaction to the “Brexit” decision was swift and severe with the Pound falling sharply along with global equity markets, while safe have assets such as government bonds and gold rose in value. In the following days however equity markets recovered much of their lost ground as major central banks, most notably the Bank of England and European Central Bank, all indicated that they were prepared to ease policy further to offset the potential negative impact on growth of the Brexit decision. There was considerable volatility in equity markets over the course of the month. The pivotal US market finished marginally up by 0.3% although surprisingly, the UK market was actually up 4.7% for the month having rallied strongly in the lead up to the referendum on the expectation of a victory for the Remain campaign. On the Continent, markets fared much worse with Germany down 5.7% and France down 6% on fears concerning the potential for other member countries to leave the EU in the wake of the UK decision. Across Asia, the Japanese market was sharply down by 9.6% on the concerns about the impact on exports from the strong Yen, which is up by 18% this year against the USD. The Australian market was down 2.4% with losses limited by a stronger resource sector buoyed by firmer commodity prices while listed property trusts once again demonstrated their defensive qualities improving by 3.5%. Gold rose 9.3% reflecting its status as a safe haven in times of uncertainty while government bonds were keenly bid, the yield on 10 year US Treasuries fell 38 basis points to finish the month at 1.47% while Australian 10 year bond yields fell 30 basis points to close just below 2%.