Politics Take Center Stage

It’s hard to remember a financial year where political events were so prominent in determining the direction of financial markets.

Firstly, the Brexit vote in the UK took everyone by surprise as the surge in British populism was missed by the pundits and raised concerns about both the impact on the UK economy and the prospect of a gradual disintegration of the continental EU if other countries chose to follow suit.

Perhaps the most stunning electoral upset in history was the November election of Republican candidate Donald Trump as the 45th President of the US. The US equity market rallied strongly on the prospect that tax cuts, infrastructure spending, and reduced regulation would lift the US out of its low growth trajectory and boost corporate profits. In the last few months however the tide of populism has been halted by the election of more moderate pro-EU governments in Holland and France.

In Australia, Prime Minister Malcolm Turnbull surprisingly called a double dissolution election, which meant the full Senate was up for election rather than the normal half Senate. While Coalition government was returned with a razor thin majority in the lower House, the composition of the Senate went from being difficult to manage to dysfunctional with minor parties and independents making the task of passing any serious economic reform next to impossible. As a consequence, the May Federal budget produced very little to stimulate a struggling economy.

Stocks delivered in spades, bond returns were poor

Despite the newspaper headlines describing global turmoil surrounding referendums, elections and geopolitical events, the financial year proved to be an exceptional year for equity markets with strong returns recorded by most major exchanges. Share prices were inflated by easy monetary conditions, and the prospect of improving global growth and stronger corporate profits.

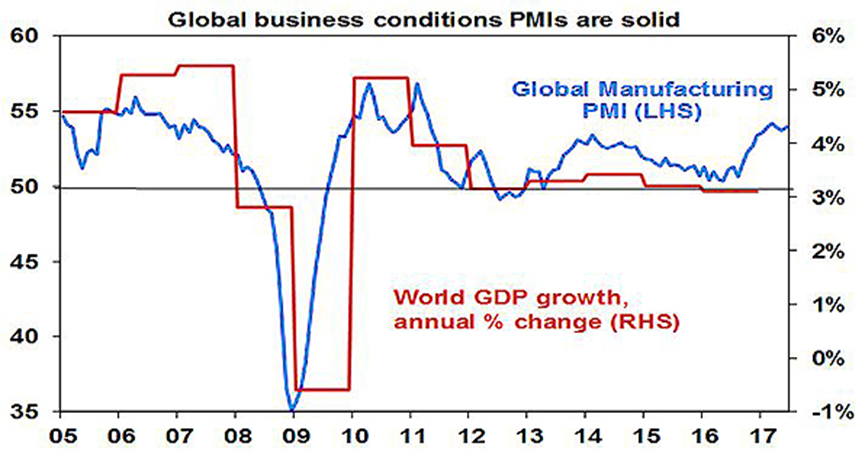

Leading indicators of growth such as the Global Manufacturing Purchasing Managers Index (PMI) shown below, are pointing to a pick-up in global growth for the year ahead.

Amongst the major markets, Japan delivered 26%, Germany 26%, the UK 11% and the bell weather US market rose a healthy 15%. Australia was a relative laggard amongst its global peers but still managed to return 13% with generous dividends contributing a good proportion of this return.

Things were not so rosy for defensive assets such as government bonds which suffered from the gradual tightening of global monetary conditions led by the US which has both discontinued its QE program and tightened cash rates on 4 separate occasions. As discussed in length in a recent monthly report, sovereign bond markets are likely to deliver poor investment returns for many years to come meaning that investors are paying much too high a price for the capital security they offer.

It’s worth remembering that the world’s major government bond markets such as the US, Japan and across Europe have been grossly distorted by large-scale Central Bank buying programs to ease liquidity conditions and stimulate growth and inflation. This has pushed global bond yields down to artificially low levels and in some case to negative levels which is clearly unsustainable. Rising bond yields reduces the capital value of bonds, which can more than offset the income return provided by coupon payments, as was the case for Australian bonds which returned -0.8% over the past 12 months.