Equity markets continued to move higher in May as the very easy global liquidity conditions that have prevailed for some time now, continued to be the driving force for financial markets.

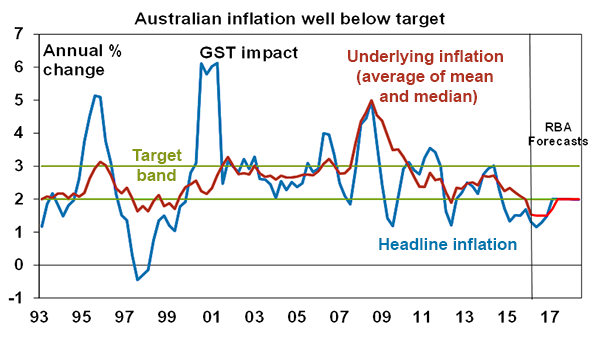

In Australia, a surprise 0.25% rate cut by the RBA in early May propelled the local market 3.1% higher with Industrials up a healthy 4.5% but the resource sector fell by 5.3% on concerns about the outlook for commodity prices and a sharp fall in BHP following litigation over a mining accident in Brazil. The interest rate sensitive listed property trust sector was up 2.6% as investors sought out higher yielding alternatives to cash and fixed income. The Australian Federal Government also handed down their pre-election Budget which had very little impact on the market as most policy initiatives were well telegraphed in advance. The US equity market edged 1.8% higher despite growing conviction about a near term rate hike, while European markets led by Germany firmed by 2.2%. The UK market continues to be weighed down by concerns of a possible Brexit, advancing by just 0.3%. Australian 10 year bonds returned a solid 1.3% for the month while the $A fell 5.1% against the $US, once again driven by the rate cut which narrowed the interest rate differential with the US. The oil price once again posted strong gains up 6.9% to finish the month at $49 a barrel. Oil has now risen by more than 85% since touching a 12-year low in February on signs the global surplus is easing.